Getting travel insurance for cancer is not as simple as picking a standard policy off a comparison website. The key is to look for a specialist insurer who genuinely understands your medical history. They're equipped to offer comprehensive cover that will actually protect you from what could be cripplingly expensive medical bills overseas.

Why Specialist Travel Insurance Is Non-Negotiable

A cancer diagnosis, whether you're in treatment or years into remission, fundamentally changes your travel planning. It’s a dangerous misconception to think that a standard, off-the-shelf policy will have your back. In reality, these policies are built for travellers with no significant health issues and are often packed with broad exclusion clauses that could render your cover useless just when you need it.

For anyone who has been through cancer, a specialist policy isn't an optional extra; it's an absolute must. These policies are carefully underwritten by providers who get the complexities of oncology. They’ll ask the right, detailed questions to assess your personal situation accurately, making sure your cover is both valid and robust enough for your trip.

The Financial Risks Of Inadequate Cover

The financial fallout from travelling with the wrong insurance can be catastrophic. Medical care abroad, especially in places like the USA, comes with a staggering price tag. If your standard policy excludes claims related to cancer, you'd be left footing the entire bill for any medical issue that arises—even if it seems completely unrelated to your cancer history.

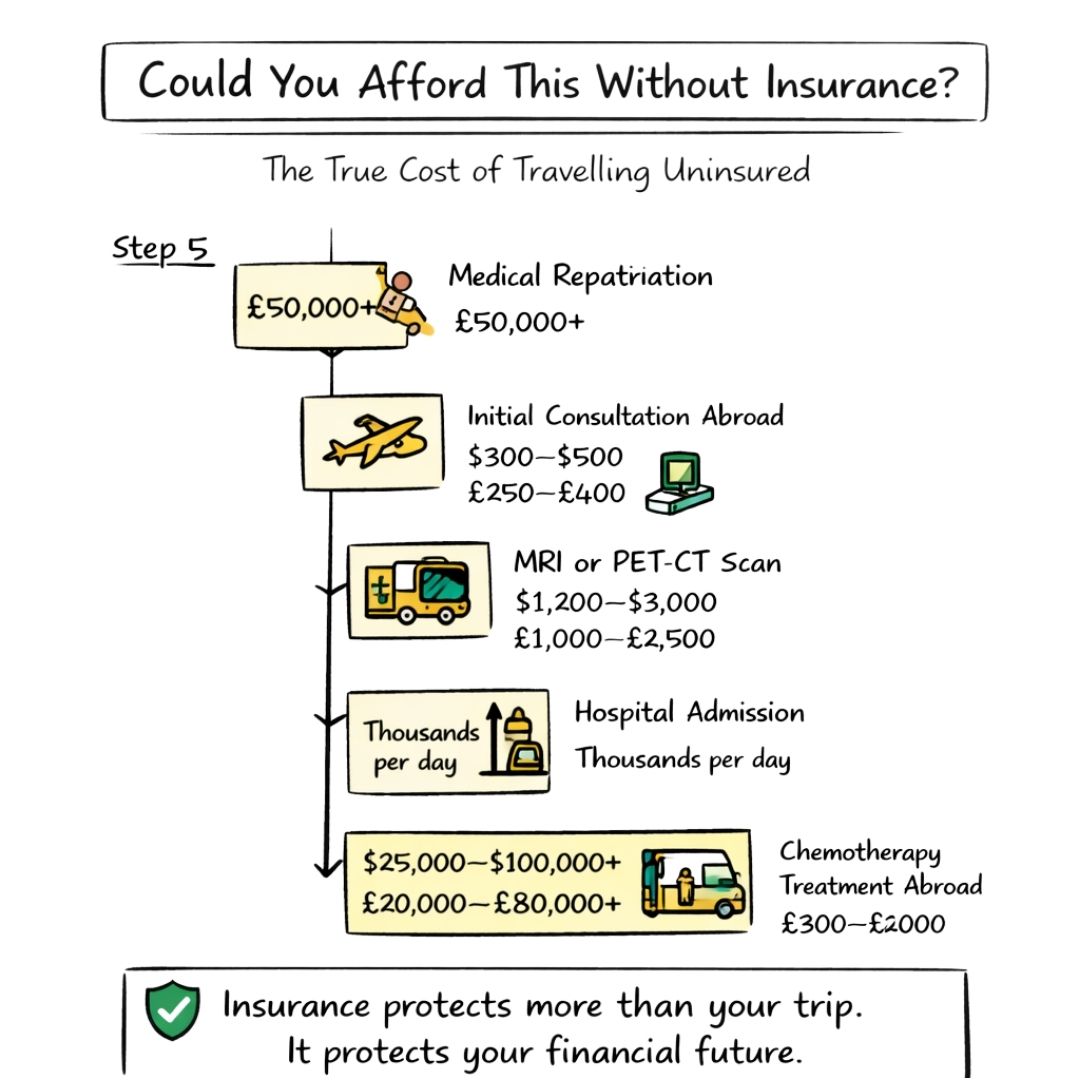

Just to put it in perspective, the costs can escalate frighteningly fast. An initial chat with an oncologist abroad could set you back $300 to $500 (£250 to £400), while a single MRI or PET-CT scan can run anywhere from $1,200 to $3,000 (£1,000 to £2,500). A full course of chemotherapy? That could easily hit $25,000 to $100,000 (£20,000 to £80,000), and sometimes much more. This ITIJ report details just how high these costs can climb, which is why having the right cover is so critical.

Peace Of Mind Is Priceless

Beyond the numbers, the right insurance gives you something invaluable: peace of mind. It allows you to actually switch off and enjoy your holiday, secure in the knowledge that you’re protected if something unexpected happens. This is even more important when you consider that some cancer treatments can affect your immune system, potentially leaving you more vulnerable to infections while you're away.

A good specialist policy is designed to cover a range of real-world scenarios, including:

Emergency medical expenses that are either directly or indirectly linked to your cancer.

Repatriation to get you home if it becomes medically necessary.

Cancellation or curtailment if you need to cancel or cut short your trip because of your health.

Cover for lost medication or essential medical equipment.

Securing the right travel insurance is about far more than just ticking a box. It’s about protecting your health and your finances, so you can focus on making wonderful memories without the "what if" cloud hanging over your holiday.

Getting The Details Right: Pre-Existing Conditions and Full Disclosure

When you're looking for travel insurance after a cancer diagnosis, how you handle your medical history is everything. Insurers define a pre-existing condition far more broadly than you might think, covering not just the cancer itself but a whole web of related health issues. Honestly, getting this part right is the single most important step you'll take.

Think of it like building a house. Your medical declaration is the foundation. If that foundation is shaky or has missing pieces, the entire structure, your insurance policy, is at risk of collapsing right when you need it to stand strong.

What Insurers Actually Mean By a Pre-Existing Condition

Most people are surprised by just how comprehensive an insurer's definition of a pre-existing condition is. It goes well beyond your current diagnosis or whether you're in active treatment. It's a full-spectrum look at your entire cancer journey.

You’ll almost always need to declare:

Your primary cancer diagnosis, including the specific type and stage.

Any secondary or metastatic cancers, even if they're currently stable.

All treatments you’ve had in the last few years—think chemotherapy, radiotherapy, surgery, or immunotherapy.

Any ongoing medication, from hormone therapies to targeted drugs.

Pending investigations on the horizon, like scheduled scans, blood tests, or consultations.

Even symptoms you've noticed but haven't had a chance to discuss with your doctor yet.

This isn't about being nosy. It’s how an insurer accurately assesses the risk to offer a policy that provides real, dependable protection. Holding back information, even by accident, can be classed as non-disclosure.

The Real Cost of Not Declaring Everything

The consequences of failing to provide a full picture of your health can be devastating. If you make a claim and the insurer finds out about an undeclared condition, they have the right to void your policy entirely.

That means they can act as if the policy never existed in the first place, refusing to cover your medical bills, emergency transport home, or cancellation costs. You'd be left personally responsible for every single penny, a bill that could easily spiral into tens or even hundreds of thousands of dollars or pounds.

Imagine this scenario: someone who had breast cancer five years ago and considers themselves "cured" decides not to mention it. On holiday, they trip and break their leg. The hospital takes a routine medical history and notes the past cancer diagnosis. The insurer could argue that had they known, they would have set a different premium or even declined cover. They could then refuse the claim for the broken leg, leaving the traveller with a massive medical bill for a completely unrelated accident.

The golden rule is simple: when in doubt, declare it. It’s always, always better to overshare than to hold back. Total honesty is what makes your policy a safety net you can actually rely on.

How Your Cancer Type and Stage Influence Your Policy

Insurers don't just lump all cancers together. They analyse each type and stage differently because every situation carries a unique risk profile. A localised, early-stage cancer treated successfully several years ago is a world away from an advanced, metastatic cancer that needs ongoing management.

An underwriter will dig into the specifics, considering things like:

Stability: Is your condition stable, in remission, or actively progressing?

Complication Risk: Does your cancer type or treatment raise the chances of other issues, like infections or blood clots?

Prognosis: What is the long-term outlook according to your medical team?

This is precisely why their medical screening questionnaires feel so in-depth. They're building a complete, accurate picture to price the premium and tailor the cover to you. It's important to be clear on understanding how medical conditions impact your coverage and to be upfront with your answers. This is your side of the bargain, and it ensures the insurer can hold up theirs when it matters most.

How To Find And Secure The Right Travel Insurance Policy

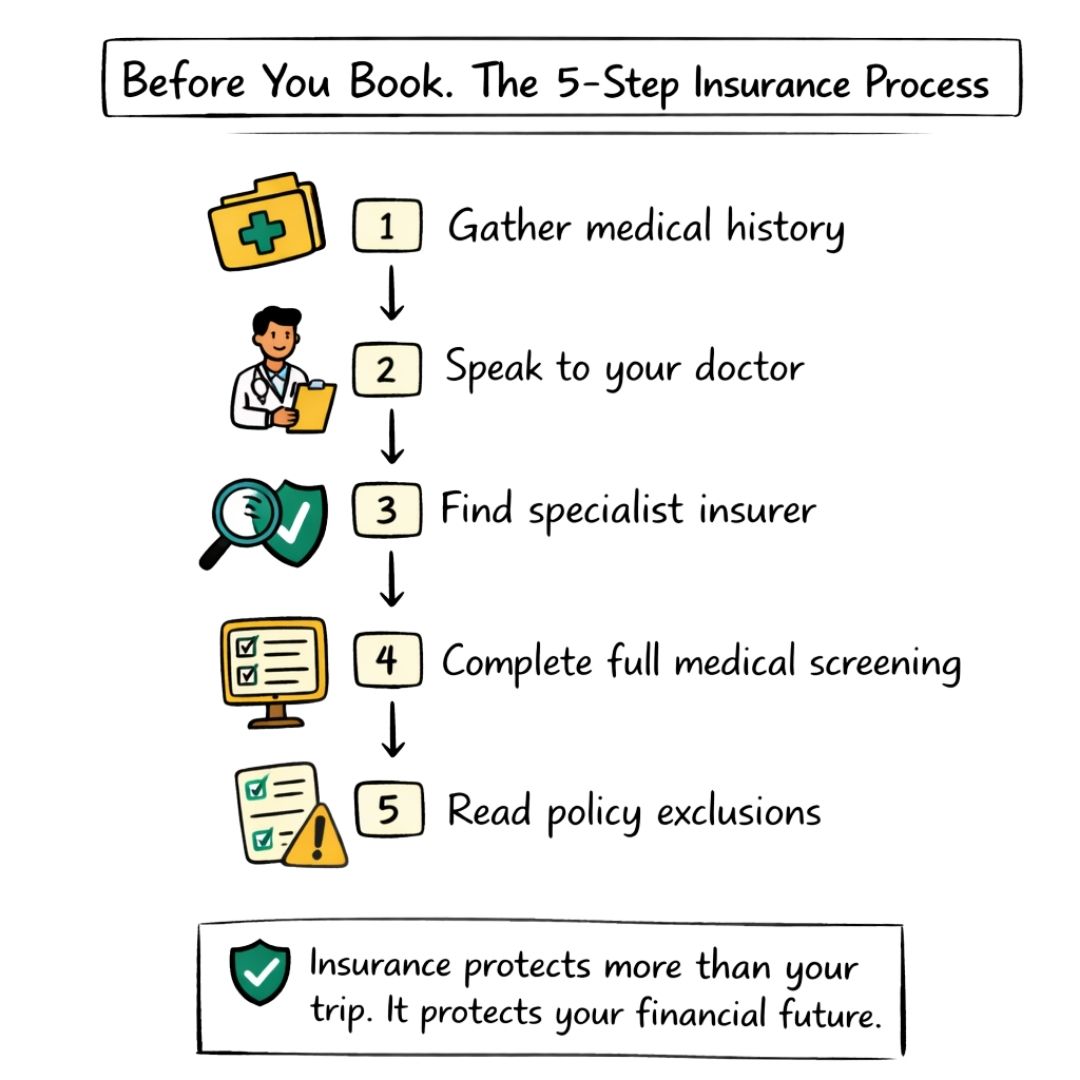

Finding the right travel insurance for cancer can feel daunting, but breaking it down into a few practical steps makes it far more manageable. The key is to be methodical. If you approach it with the right information and a clear plan, you can find a policy that gives you genuine peace of mind.

Before you even think about getting quotes, the most important thing you can do is gather all your medical details. Insurers need a clear, organised picture of your health, and having this ready from the start will make the whole process smoother and ensure any quotes you get are actually accurate.

Prepare Your Medical Information

Think of this as creating your personal medical brief. Before you pick up the phone or start filling in online forms, compile a clear, detailed summary of your cancer journey. It’s crucial to be precise, as any inconsistencies could cause serious issues if you need to make a claim down the line.

Your summary should pull together a few key things:

Your exact diagnosis: Be specific about the type of cancer, its grade, and stage.

Important dates: The date you were first diagnosed is a must-have.

Treatment history: List every surgery, round of chemotherapy, radiotherapy, or immunotherapy you've had. Make sure to include the start and end dates for each.

Current status: Are you in remission? Still undergoing active treatment? Or perhaps on a 'watch and wait' protocol?

Medications: Create a complete list of everything you're currently taking, including the dosages.

Having this information at your fingertips saves you from frantically searching for details while you're on a call or halfway through an application. It shows the insurer you're organised and on top of your condition, which can really help streamline their assessment. This prep work is also a great exercise for your own records and for discussions with your cancer care team.

Know Where To Look For Cover

Forget the standard comparison websites. They're built for speed and volume, which means they often automatically screen out anyone with a complex medical history. Trying to use them can leave you feeling frustrated and with the false impression that cover is either unavailable or impossibly expensive.

Your best bet is to focus your search on providers who genuinely specialise in travel insurance for pre-existing medical conditions. These insurers have underwriting teams who actually understand the nuances of a cancer diagnosis.

Here are a few avenues to explore:

Specialist Insurance Brokers: These experts do the legwork for you, tapping into a wide range of policies from different underwriters that you wouldn't find on your own.

Cancer Charities: Many organisations partner with or can recommend insurance providers who have a solid track record of helping people in your situation.

Direct Specialist Insurers: A growing number of companies now market themselves directly to people with medical conditions. A quick search for "travel insurance for cancer patients" will bring up several reputable options.

The reality is that as more people live with and beyond cancer, the insurance industry is being forced to adapt. Projections show that in some countries, as many as one in two people will face a cancer diagnosis in their lifetime. Already, the number of people living with cancer in the UK has jumped from nearly 3 million to almost 3.5 million in just a few years. This growing demand is making fair and accessible insurance more critical than ever. You can read more about the need for specialised financial protection on wecovr.com.

The Medical Screening Process

Once you’ve identified a potential insurer, you'll go through a medical screening. This is simply a set of detailed questions about your health, which you can usually complete online or over the phone. When it comes to this part, total honesty isn't just a good idea—it's a contractual requirement.

The questions will be very specific, digging into the details you've already prepared in your medical summary. They’ll likely ask about recent hospital visits, any pending test results, or changes to your treatment plan. Each answer you give helps the insurer calculate your individual risk and, in turn, your premium.

Remember, the screening isn't a judgement call on your health. It’s a fact-finding exercise to make sure the policy they offer you is right for your circumstances and will actually be valid if you need it.

It's okay to say "I don't know" if that's the truth, but it's far better to have the correct information from your doctor beforehand. Being completely upfront and accurate is the only way to be certain your policy will have your back when it really counts.

Decoding Your Policy: What Is and Is Not Covered

Once you’ve gathered a few quotes, the real work begins. It’s tempting to just look at the price, but an insurance policy is a legal document, and the language can feel dense and impenetrable.

Taking the time to properly understand what’s covered—and just as importantly, what’s not—is the only way to be sure the policy is worth more than the paper it's printed on. The cheapest option is almost never the best one, especially when you're looking for travel insurance for cancer. The real value is buried in the details.

The Three Pillars of Travel Insurance Cover

At its heart, a specialist policy is there to shield you from major financial shocks. For anyone with a history of cancer, this protection really hinges on three critical areas. Getting your head around how they apply to you is essential.

Emergency Medical Expenses: This is the absolute cornerstone of your cover. It’s what pays for any emergency medical treatment you need while you're away. It's not just for cancer-related problems; it covers everything from a sudden infection to a broken ankle. The crucial part is that because you’ve declared your full medical history, the insurer has agreed to cover emergencies that might be linked, directly or indirectly, to your cancer.

Cancellation and Curtailment: Think of this as protecting the money you've spent on your trip. If your doctor advises you not to travel because of a change in your health, this feature lets you claim back non-refundable costs like flights and hotels. Curtailment is similar—it covers your costs if you have to cut the holiday short for an approved medical reason.

Medical Repatriation: If you become seriously ill abroad, this covers the often eye-watering cost of getting you home safely. This could be something as simple as a business-class seat for more comfort, or it could mean a full air ambulance with a medical crew on board. That sort of service can easily run into tens of thousands of dollars or pounds.

Reading Between the Lines: Common Exclusions

Knowing what your policy covers is only half the battle. You also need to be crystal clear on what it doesn't cover. Every policy has exclusions, and finding out about one after you’ve had a problem is a nightmare scenario. They aren't hidden in secret clauses; they're laid out in the policy wording for you to read.

Be on the lookout for these common exclusions:

Travelling Against Medical Advice: If your doctor has specifically told you that you are not fit to travel, any claim you make will almost certainly be rejected. Simple as that.

Terminal Prognosis: Many standard insurers won't cover anyone travelling with a terminal diagnosis and a short life expectancy. However, some specialist providers absolutely will, though it might be for a single trip to a specific destination.

Claims for Undeclared Conditions: We’ve said it before, but it bears repeating. If you don't declare your full medical history, any claim related to it will be denied. This is the single biggest reason claims are refused.

Elective Treatment Abroad: Travel insurance is for unforeseen emergencies. It will not cover any planned medical treatment, check-ups, or tests you decide to have while on your holiday.

Reading your policy document isn't just a suggestion—it's a critical step. Pay close attention to the sections on 'General Exclusions' and the specific terms related to pre-existing conditions to ensure there are no surprises.

For those managing ongoing health needs, such as palliative care, understanding policy limits is especially important. Our guide on the benefits of palliative care can offer context on managing symptoms, which is a key consideration when planning travel.

Comparing Levels of Cover

Now that you know what to look for, let's break down those different tiers of cover you'll see in your quotes. Insurers often present them as Bronze, Silver, and Gold packages, and while the price varies, so does the level of protection. This table shows what those differences really mean.

Key Policy Features For Cancer Patients Explained

This table breaks down essential travel insurance features, explaining what they cover and why they are critical for someone with a cancer diagnosis.

Policy Feature

What It Covers

Why It's Important For You

Emergency Medical Cover

Hospital bills, ambulance costs, doctor's fees, and emergency treatment for unforeseen medical events abroad.

This is non-negotiable. You need a high limit (ideally $10 million / £10 million+) to cover potential complications, even in countries with reciprocal healthcare.

Cancellation & Curtailment

Reimburses pre-paid, non-refundable travel and accommodation costs if you have to cancel or cut your trip short due to a medical emergency.

Your health can be unpredictable. This protects your financial investment if your doctor advises against travel or you need to return home early.

Medical Repatriation

The cost of getting you back to your home country, which can range from a scheduled flight with a medical escort to a private air ambulance.

A medical evacuation can cost $60,000 / £50,000 or more. Without this cover, you could be facing a life-changing bill.

24/7 Emergency Assistance

A dedicated helpline you can call from anywhere in the world for medical advice, assistance, and to coordinate your care.

In a crisis, having an expert on the phone who can speak the local language and liaise with hospitals on your behalf is invaluable.

Ultimately, choosing the right level comes down to your personal situation and the trip you’re taking. For a short city break in Europe, a solid mid-range policy might be all you need. But for a two-week trip to the USA, where healthcare costs are astronomical, settling for anything less than the highest level of medical and cancellation cover would be a false economy.

Confirming Your Fitness To Travel With Your Medical Team

Before any insurer will even consider offering you a policy, they need one crucial thing: confirmation from your medical team that you are fit to travel. This isn't just a box-ticking exercise. It's the cornerstone of your entire travel insurance for cancer, assuring the insurer that your doctor sees no immediate reason why you'd need medical help while you're away.

Think of this official sign-off as your proof that you're not travelling against medical advice. That's a standard exclusion in almost every policy, and ignoring it would render your cover useless right when you need it most. It shows you're taking a responsible, proactive approach, which is exactly what insurers want to see.

What Does "Fit To Travel" Really Mean?

The phrase "fit to travel" can feel a bit ambiguous, but in the world of insurance, it's quite specific. It means your GP or oncologist has looked at your current health, recent treatments, and the details of your trip, and concluded that your condition is stable enough for you to go.

It's a decision based on context. A relaxing weekend in Paris places very different demands on your body than a long-haul flight to Australia, followed by an active tour. Your doctor weighs up the specifics of your itinerary against your health, making this conversation an absolutely vital part of your planning.

This step has become even more critical given the immense pressure on some national healthcare services. In England, for instance, the NHS has struggled to meet its 62-day referral-to-treatment target for cancer for several years. The reality is that a significant number of people diagnosed with cancer in the UK have endured dangerously long waits for care. These delays add another layer of complexity to travel planning and underscore the importance of getting everything right with your insurance. You can find more details on these NHS pressures on wecovr.com.

Having a Productive Conversation With Your Doctor

To make this consultation truly effective, you need to go in prepared. Your doctor can give you the best advice only when they know exactly what your trip involves. A little bit of prep work ensures you cover all the important points and leave with the confidence you need for your insurance application and your holiday.

It's always a good idea to bring a written list of questions. The goal here is to get a clear picture of any potential risks and, more importantly, how you can manage them while you're away.

Here are some key questions to get the conversation started:

Given my current health, do you have any specific concerns about this particular trip?

Are there any activities you think I should avoid, like swimming or long hikes?

Do I need any extra vaccinations, and are they safe for me to have right now?

Would it be helpful to carry a letter that summarises my diagnosis and current medications?

What specific symptoms should I watch for that would mean I need to see a doctor abroad?

How can I best manage potential side effects, like fatigue or sun sensitivity, in a new environment?

This conversation is a partnership. Your doctor brings the medical expertise, but you are the expert on your travel plans. Together, you can create a strategy that prioritises your health and safety.

This kind of collaborative planning is particularly important if you're in a post-treatment phase, as side effects can linger for quite some time. Our guide on the recovery from chemotherapy provides some useful insights into what you might expect. Getting that green light from your doctor is the final, essential piece of the puzzle, allowing you to travel with peace of mind, knowing you are properly protected.

Common Questions About Travel Insurance for Cancer

Once you start looking into travel insurance after a cancer diagnosis, a lot of very specific, practical questions tend to pop up. Even when you’ve got the basics down, you might still wonder how the rules apply to your particular situation. This section tackles some of the most pressing queries we hear, giving you clear, straightforward answers to help you feel confident in your decisions.

Perhaps the most common and fundamental question is, "If I Had Cancer Can I Still Get Travel Medical Insurance?" The short answer is yes, you can. But the devil is always in the detail. Let's dig into some of the key scenarios you might be wrestling with.

Can I Get Travel Insurance If I Have A Terminal Diagnosis?

This is a tough one, but it’s not always a closed door. Getting travel insurance with a terminal diagnosis is certainly challenging, and mainstream insurers will almost always decline to offer cover. From their perspective, the risk of a medical emergency or trip cancellation is just too high for a standard policy.

That said, some specialist providers are set up to handle these complex cases. They will take you through a very detailed medical screening, focusing on your current stability, your doctor’s view on your life expectancy, and the nature of the trip you’re planning.

If you do manage to find cover, here’s what you should probably expect:

Single-Trip Policies Only: Insurers will almost certainly limit cover to one specific trip rather than an annual multi-trip policy.

Destination Limitations: You may find there are restrictions on where you can go. Insurers often feel more comfortable with destinations where healthcare costs are lower.

Higher Premiums: Be prepared for the cost to be significantly higher, as it has to reflect the increased level of risk the insurer is taking on.

The absolute key here is total honesty, both with your insurer and your own medical team. Your doctor must agree that you are fit to make the journey, and you must be completely transparent with the insurer about your prognosis.

What If My Health Changes After I Buy The Policy But Before I Travel?

This is a critically important point that catches many people out. Your responsibility to the insurer doesn't stop the moment your payment goes through. You have an ongoing duty to tell them about any changes to your health that happen between buying the policy and the day you set off.

What counts as a "change in health"? It’s broader than you might think:

A new diagnosis, whether it's related to the cancer or not.

A shift in your treatment plan, like starting a new medication.

Your doctor sending you for new tests or investigations.

Experiencing new symptoms or finding that existing ones have got worse.

If you don't report these changes, your policy could be invalidated. The insurer needs to reassess the risk with this new information. It might mean your premium goes up, they add a new exclusion, or in some cases, they might have to withdraw cover. It feels like a hassle, I know, but it’s the only way to be sure your policy will actually protect you if you need it.

Always contact your insurer immediately if your health status changes before your trip. It's far better to have an honest conversation and know where you stand than to travel with a policy that may no longer protect you.

Do I Still Need To Declare Cancer If I Have Been In Remission For Years?

Yes, you absolutely do. This is a non-negotiable. Insurers will typically ask about any medical conditions you've had in the last 5 to 10 years, and some will ask if you've ever had a certain condition. Even if you've been in remission for a very long time and feel fully recovered, that initial diagnosis is still a 'material fact' that the underwriters need to know about.

Withholding that information, even if you think it's irrelevant, is called non-disclosure. If you had to make a claim for something completely unrelated—say, you slipped and broke your ankle—the insurer would investigate your medical history. If they discovered an undisclosed cancer diagnosis, they could void your entire policy on the spot, leaving you to foot the bill yourself.

The good news is that declaring a cancer diagnosis from many years ago, especially with a long period of stability and no further treatment, may not even affect your premium. For many insurers, that stability significantly lowers the perceived risk. It's always, always better to be upfront.

Why Is Insurance More Expensive For Destinations Like The USA?

The price of your travel insurance is directly tied to how much a potential medical claim could cost. And healthcare in some countries is famously, eye-wateringly expensive. The United States is the prime example, but places like Canada, the Caribbean, and some parts of the Middle East also have very high medical bills.

A policy covering a trip to the USA costs more for a few simple reasons:

No Public Healthcare for Visitors: Unlike national health systems in some countries, the US healthcare system is almost entirely private. There's no safety net for tourists; you pay for everything you get.

Astronomical Costs: A quick trip to an emergency room can run into thousands of dollars. A couple of nights on a ward with some scans or emergency surgery can easily hit six-figure sums.

High Repatriation Costs: Flying a patient back to their home country with a medical team from North America is also far more expensive than it would be from Europe.

Because the potential payout for a claim in the USA is so much higher, the premium has to reflect that greater risk. This is why you’ll often see insurers offering a "Worldwide excluding USA, Canada, and the Caribbean" policy for a lower price than a full "Worldwide" one. It’s a crucial factor to remember when budgeting for your trip.

We strongly advise you to talk with a health care professional about specific medical conditions and treatments. The information on our site is meant to be helpful and educational but is not a substitute for medical advice.

Written by Cancer Care Parcel

In a world full of conflicting and sometimes misleading information about cancer, Cancer Care Parcel stands out by offering resources backed by solid facts. Funded entirely by the sale of our products and donations, we ensure that every resource on our site is accurate, trustworthy, and focused on supporting the cancer community.